Hardware Bears Are Wrong and That’s Why I Keep Buying Apple on Repeat Alex SiroisWed, July 15, 2026 at 8:42 PM UTC 0 24/7 Wall St.Quick Read Apple&x27;s March quarter hit a revenue record of $111 billion, up 17%, backed by 8 consecutive EPS beats and a fresh $100 billion buyback. Apple&x27;s Services segment runs at a 77% gross margin, offering more predictable compounding returns than NVIDIA&x27;s uncertain AI capex payback windows. This lithium producer surpassed a $1B private valuation, joining some of America&x27;s most powerful startups.

Hardware Bears Are Wrong and That’s Why I Keep Buying Apple on Repeat

Alex SiroisWed, July 15, 2026 at 8:42 PM UTC

0

24/7 Wall St.Quick Read -

Apple's March quarter hit a revenue record of $111 billion, up 17%, backed by 8 consecutive EPS beats and a fresh $100 billion buyback.

Apple's Services segment runs at a 77% gross margin, offering more predictable compounding returns than NVIDIA's uncertain AI capex payback windows.

This lithium producer surpassed a $1B private valuation, joining some of America's most powerful startups. Now you can invest in EnergyX alongside global giants like General Motors, but only through July 16. (sponsor)

I keep clicking buy on Apple (NASDAQ:AAPL), and the hardware bears keep giving me reasons to do it again. Every quarter someone declares the iPhone cycle exhausted. Every quarter Apple hands me another record and I add to the position.

The conviction is simple. Apple sells hardware that a 2.5 billion active device installed base refuses to abandon, then rents that same base a growing bundle of high-margin services. Bears keep pricing this as a maturing phone company. I keep pricing it as a compounding annuity with a chip designer attached.

The Receipts I Keep Coming Back To

Start with the hardware. In the March quarter, iPhone revenue hit $56.994 billion, a March record, with Tim Cook citing 22% year over year growth and 99% US customer satisfaction on the iPhone 17 family. Total revenue came in at $111.184 billion, up 16.6% year over year, with double-digit growth in every geographic segment. Demand like that speaks for itself.

Then Services. Revenue reached $30.976 billion at a 76.7% gross margin. That mix keeps expanding, and it keeps decoupling Apple's earnings from any single phone launch. EPS of $2.01 beat the $1.9404 estimate, making it 8 consecutive quarters of beats.

The third leg is the capital return machine. The board authorized a fresh $100 billion buyback and lifted the dividend 4% to $0.27. Full fiscal year 2025 buybacks totaled $90.71 billion. On that shrinking share count, Apple posts 171.4% return on equity and 53.3% ROIC. Every dollar retained earns a return most companies cannot touch.

July 16 is the Final Day to Tap Into the Lithium Boom (sponsor)General Motors, POSCO, and 50,000+ everyday investors have already backed lithium producer EnergyX.

Here's why you should do the same before their July 16 investment deadline: lithium prices are up 75% this year, with demand projected to grow a staggering 5X by 2040.

Advertisement

With tech that can recover up to 3X more lithium than traditional methods, EnergyX is preparing to unlock up to 15M+ tons. Become a private-stage EnergyX investor before the July 16 deadline.

Why Not the Obvious AI Alternative

The name a tech-focused reader reaches for first these days is NVIDIA (NASDAQ:NVDA). I own some, and I keep sending fresh cash to Apple anyway. One AI-focused podcast framed the setup plainly: "the market is actually in a way saying we want to pay less for Nvidia than a company like Apple that is very growth constrained" because with Apple "you know what you're getting." The hyperscalers are pouring capex into AI infrastructure with uncertain payback windows. Apple is spending on R&D at an accelerating rate, per Cook, while still returning tens of billions to me each quarter. Predictability at this scale is rare, and I will pay for it.

The Risk I Am Not Ignoring

Greater China is the concern I sit with. The region softened to $14.49 billion in Q4 FY25 before recovering. The rebound has been fast: 33% growth in the first half of fiscal 2026 and a March record. Memory costs are climbing too, and Cook flagged a larger impact in the June quarter. Margins will feel it. The through-line still holds: an installed base compounding into a Services flywheel, backed by $62 billion in net cash. If you want to see how that Services momentum shows up in the numbers, our team pulled the receipts in 7 Stocks Powering the AI Boom (That Aren't Chipmakers).

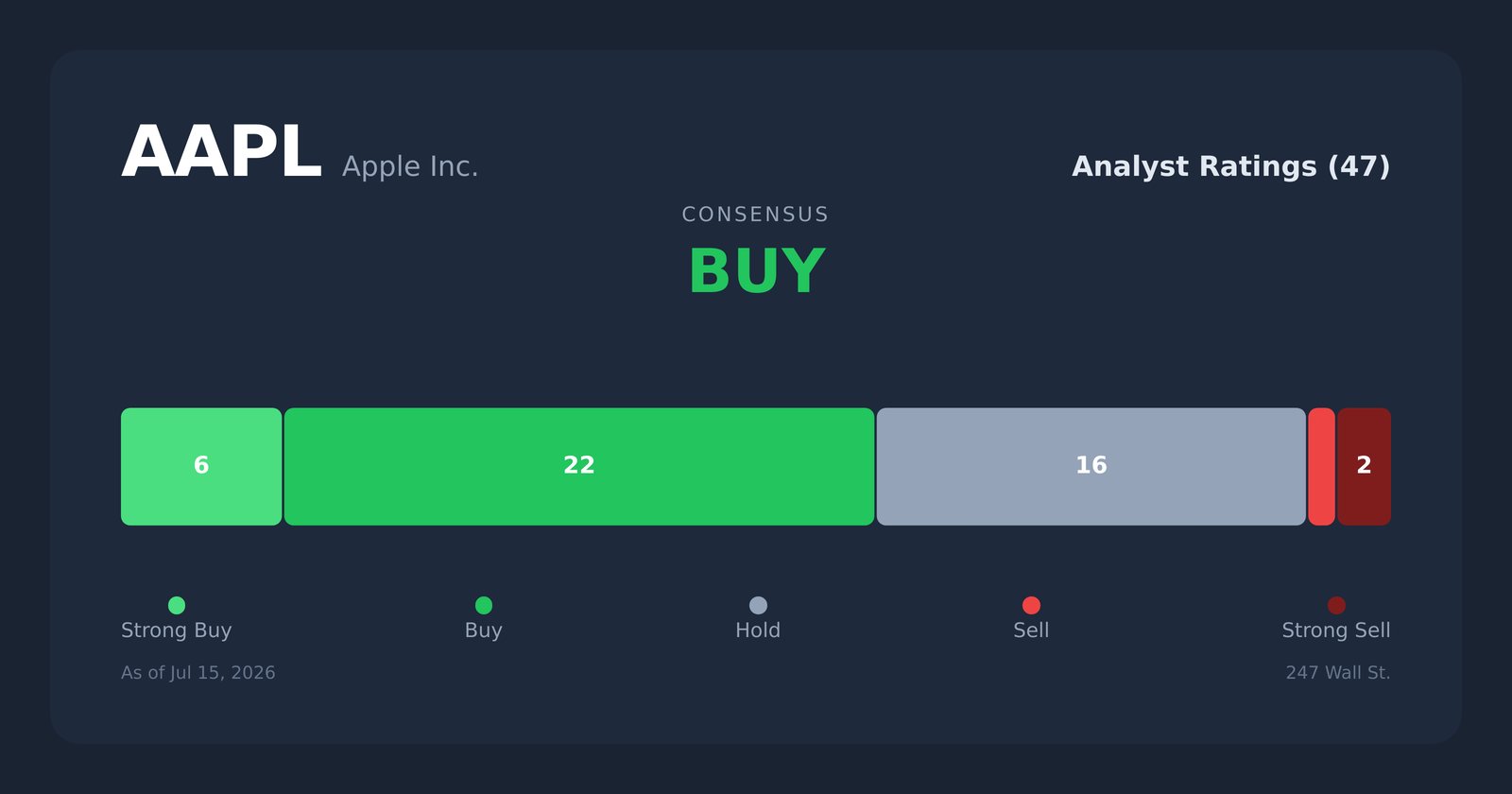

AAPL Analyst Ratings — 24/7 Wall St.Why the Buy Button Stays Active

Shares are up 51.53% over the past year and 1,300.24% over ten years at $314.86. I keep buying because the machine that produced those returns is still running: hardware people upgrade, services people pay for monthly, and a treasury that keeps buying its own stock back. The hardware bears will keep filing their obituaries. I will keep filing my trade tickets.

Meet America's Newest $1b Unicorn (Sponsor)

A US startup just passed a $1 billion private valuation, joining billion-dollar private companies like OpenAI and ByteDance. Unlike those other unicorns, you can invest in EnergyX right now; but only until July 16.

Over 50,000 people already have, along with global giants like General Motors and POSCO.

Here's why there's so much interest: EnergyX's patented tech can recover up to 3X more lithium than traditional methods. That's a big deal, as demand for lithium is expected to 5X current production levels by 2040. Become an early-stage EnergyX shareholder before the 7/16 investment deadline.

Contact editorial@247wallst.com for any questions or corrections.

Source: "AOL Money"

Source: Money

Published: July 15, 2026 at 05:18PM on Source: PRIME TIME

#ShowBiz#Sports#Celebrities#Lifestyle